Accessibility Policy

Skip to content

Oracle

Oracle Database Insider

Search

Exit Search Field

Clear Search Field

Menu

CATEGORIES

Oracle AI

Oracle Cloud Infrastructure (OCI)

Technical Solutions

Blogs Home

RSS

Oracle Database Insider

All things database: the latest news, best practices, code examples, cloud, and more

Follow:

RSS

Facebook

Twitter

LinkedIn

YouTube

Instagram

4

Take Action Today: Protect Your Oracle Database Against AI-Enabled ...

Jenny Tsai-Smith

1 minute read

Raising the Standard for Mission-Critical Availability and Security ...

Ashish Ray

11 minute read

Oracle AI Database Delivers Mission-Critical Agentic AI Built for ...

Hasan Rizvi

8 minute read

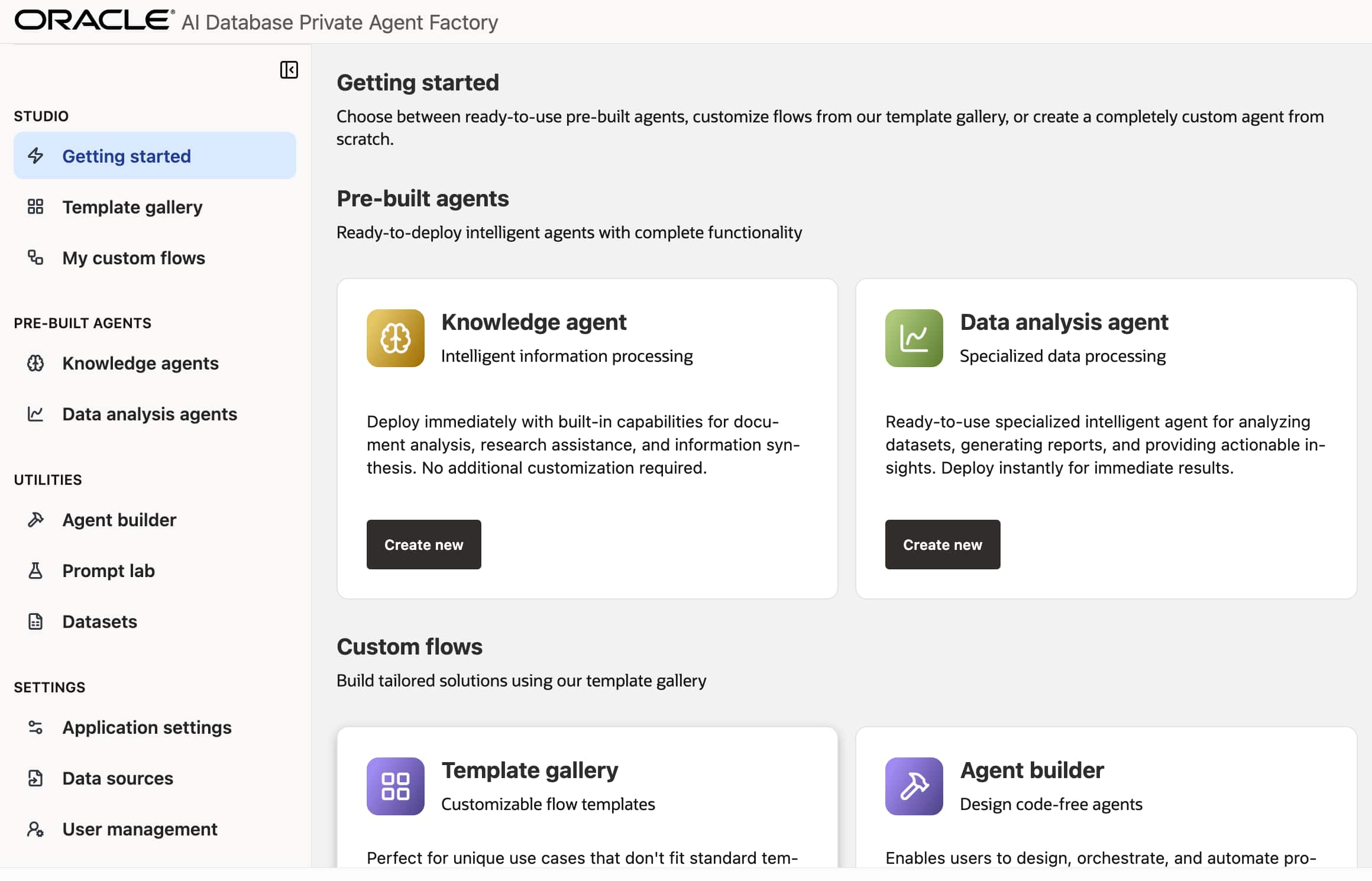

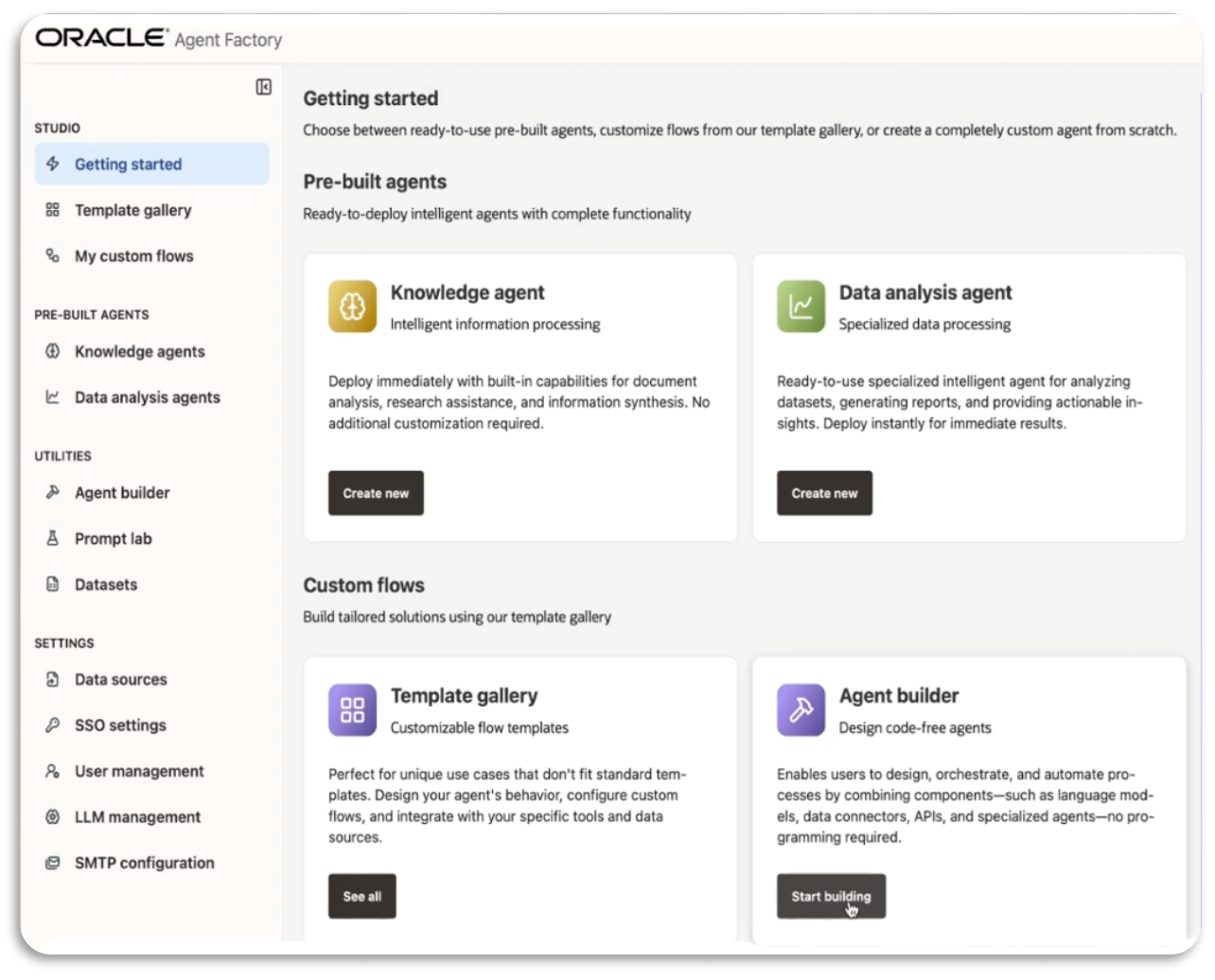

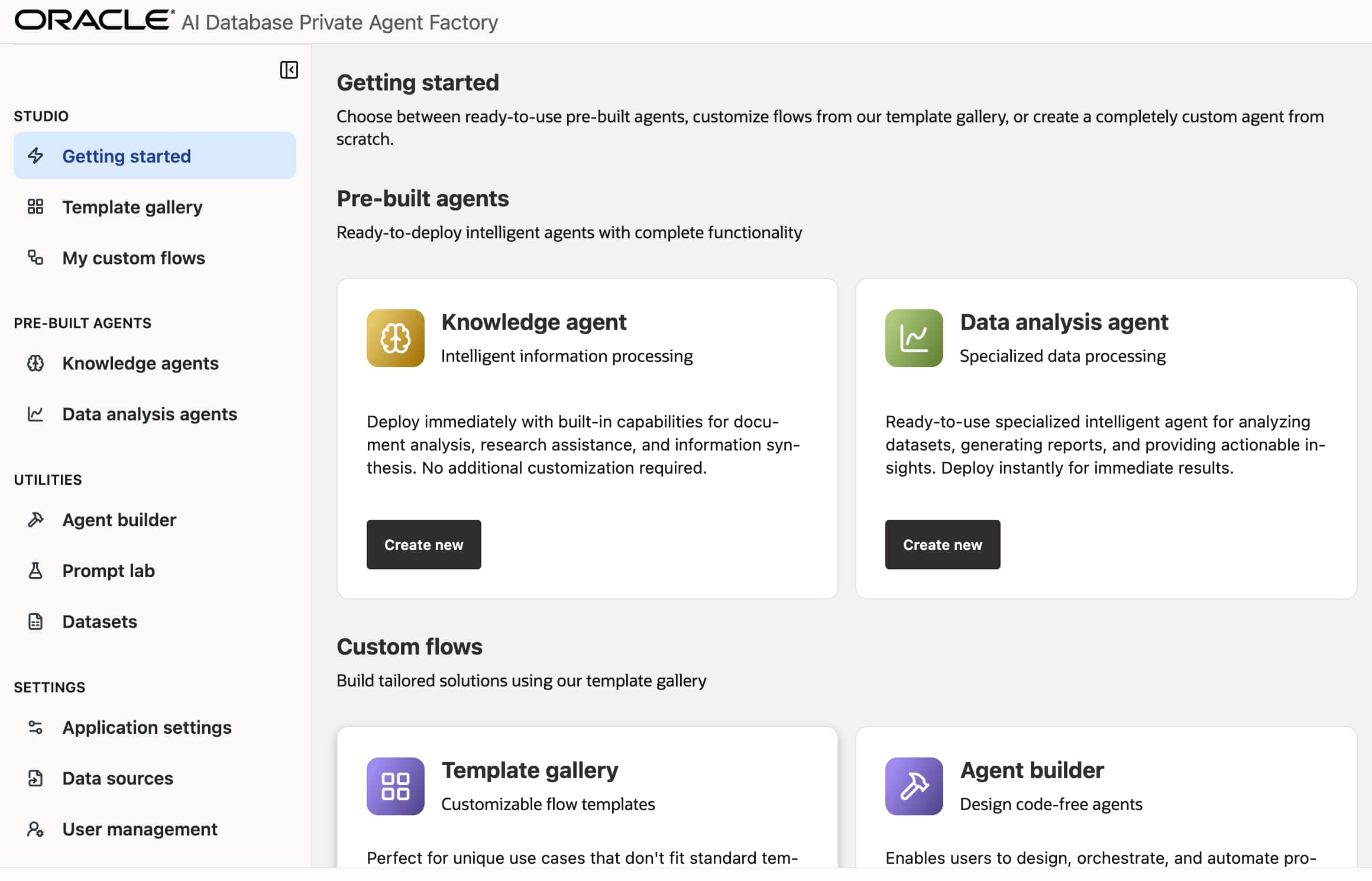

Introducing Private Agent Factory: Unlocking the Agentic AI Potential ...

Sanjay Goil

5 minute read

Search Oracle Blogs

Search this site

Type your search term and press Enter.

Receive the latest blog updates

Subscribe to our blog

Artificial Intelligence

See all

Getting Started with the Vector Index Service – Part 2

Doug Hood

12 minute read

Gain Agentic Access to Any Oracle Database in the Cloud with Native, ...

Jeff Smith

Kris Rice

8 minute read

Getting Started with the Vector Index Service – Part 1

Doug Hood

15 minute read

Oracle AI Database Private Agent Factory: Enterprise FAQ

Kumar G Varun

10 minute read

Turning Invoice Compliance into a Scalable, Auditable Workflow with ...

Kumar G Varun

6 minute read

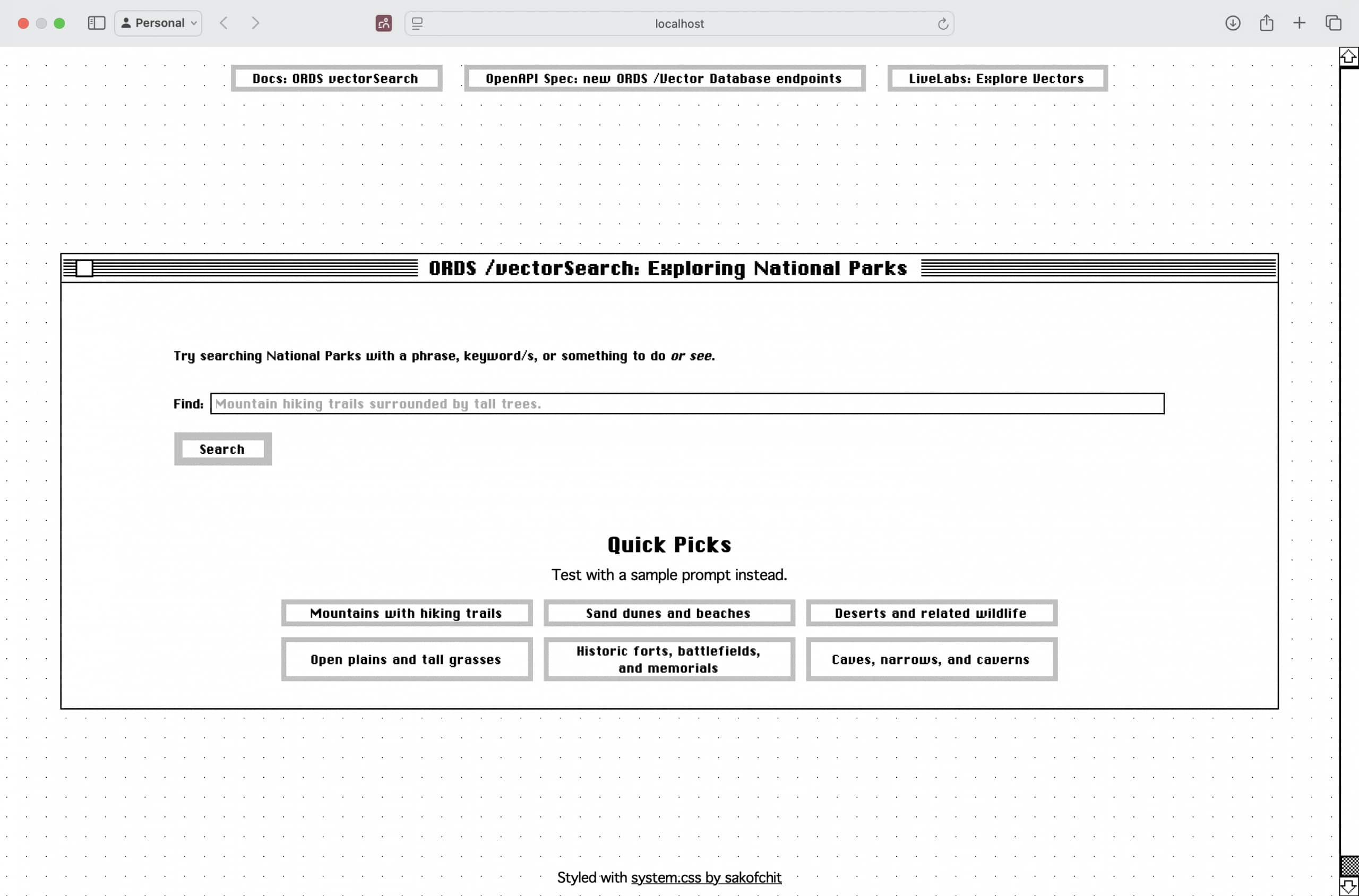

Pain Free Vector similarity search for your apps: Oracle Database ...

Chris Hoina

9 minute read

Oracle Introduces Trusted Answer Search to Deliver Fast, Accurate and ...

Sanjay Goil

Allen Hosler

6 minute read

Scaling Agentic AI: Why Transactional Messaging and a Converged ...

Nithin Thekkupadam Narayanan

4 minute read

Product News

See all

Getting Started with the Vector Index Service – Part 1

Doug Hood

15 minute read

Oracle Deep Data Security Is Now Available in Oracle AI Database 26ai

Vipin Samar

5 minute read

Oracle Customer Success Services: Patching and Upgrade Center for ...

Jenny Tsai-Smith

2 minute read

Take Action Today: Protect Your Oracle Database Against AI-Enabled ...

Jenny Tsai-Smith

1 minute read

Analyst Perspectives on Oracle AI Database Mission-Critical ...

Ron Craig

7 minute read

Raising the Standard for Mission-Critical Availability and Security ...

Ashish Ray

11 minute read

Introducing Oracle Database Security Central: Taking Control of ...

Vipin Samar

4 minute read

Announcing Oracle AI Database Operator for Kubernetes v2.1.0

Shefali Bhargava

Param Saini

Sanjay Singh

4 minute read

Vector Search

See all

Getting Started with the Vector Index Service – Part 2

Doug Hood

12 minute read

Getting Started with AI Vector Search LiveLabs Workshop Updates

Andy Rivenes

2 minute read

Getting Started with the Vector Index Service – Part 1

Doug Hood

15 minute read

Introducing the Vector Index Service

Doug Hood

3 minute read

Pain Free Vector similarity search for your apps: Oracle Database ...

Chris Hoina

9 minute read

Enterprise AI Search Needs a New Approach

Allen Hosler

4 minute read

Getting Started with Private AI Services Container

Doug Hood

16 minute read

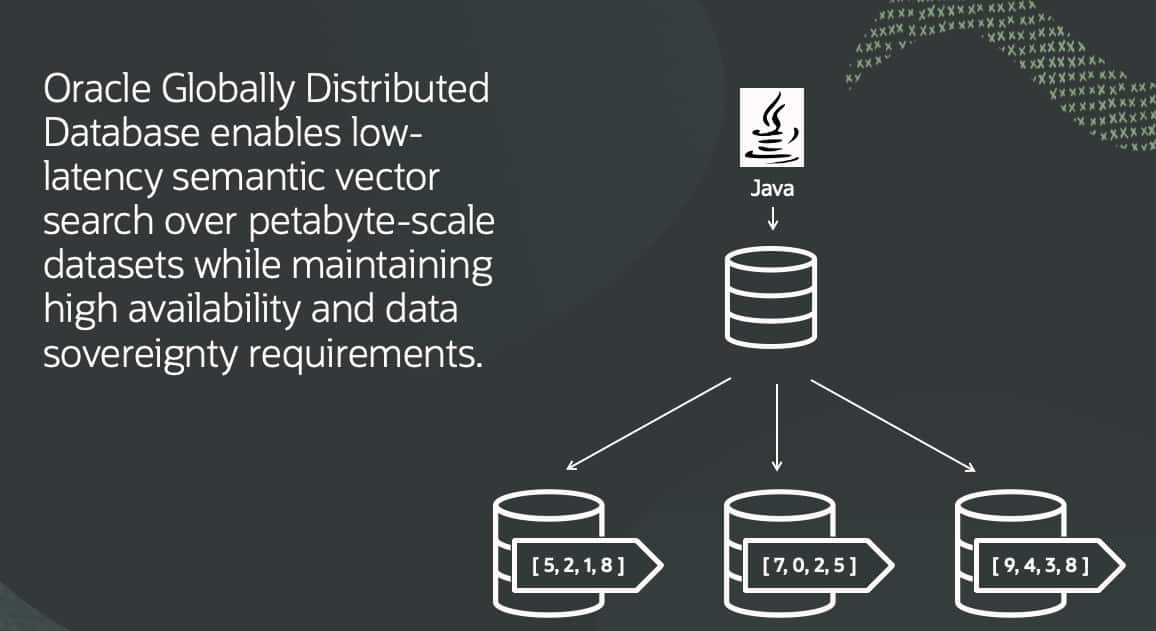

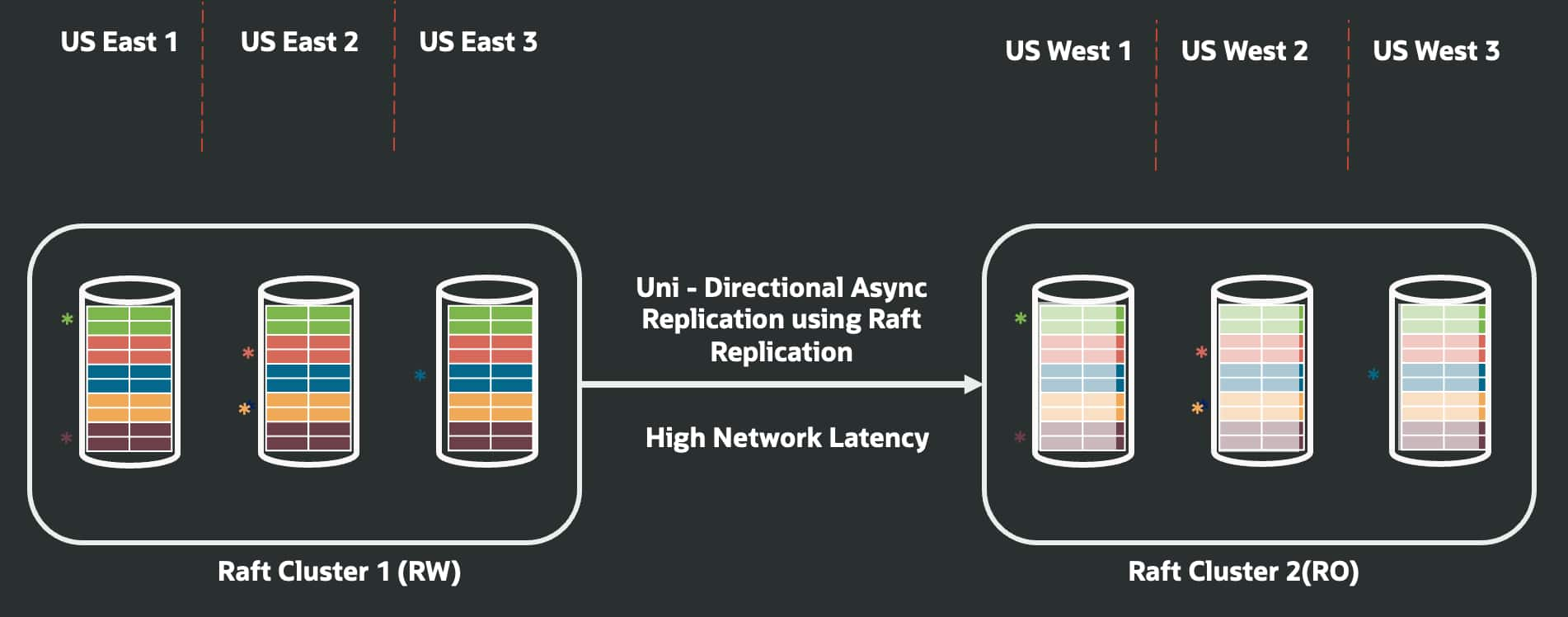

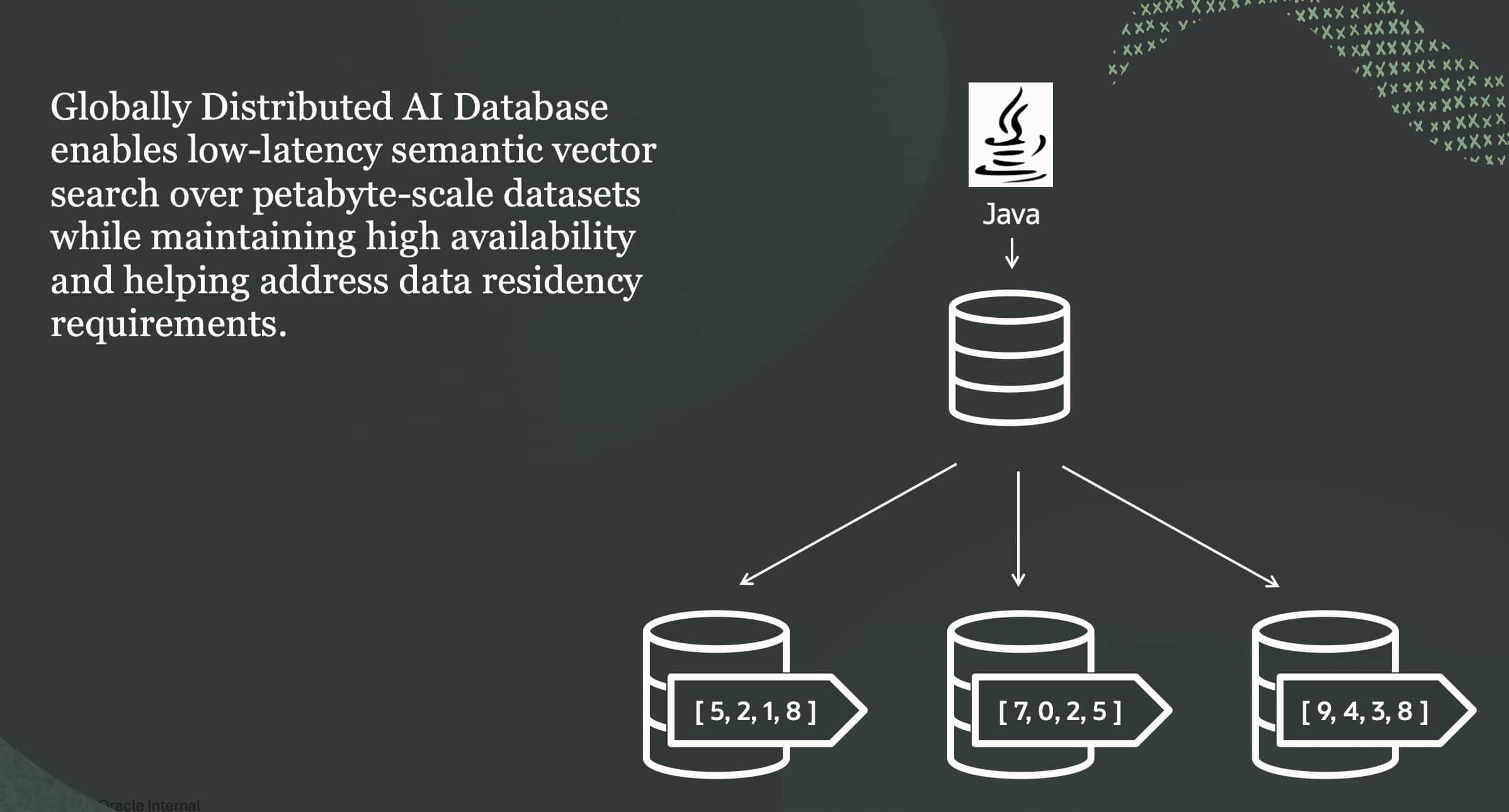

Building Scalable Vector Search with Oracle Globally Distributed ...

Kuldeep Bora

Kehinde Otubamowo

Deeksha Sehgal

7 minute read

Autonomous Database

See all

Building Trusted Generative AI Experiences with Oracle Deep Data ...

Burak Akkus

14 minute read

Cross-Platform Analytics: Oracle Autonomous AI Database Reads ...

Sathishkumar Rangaraj

9 minute read

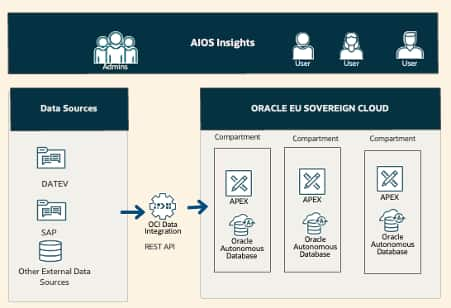

AIOS develops customized reporting and planning solutions with Oracle ...

Martina Keippel

3 minute read

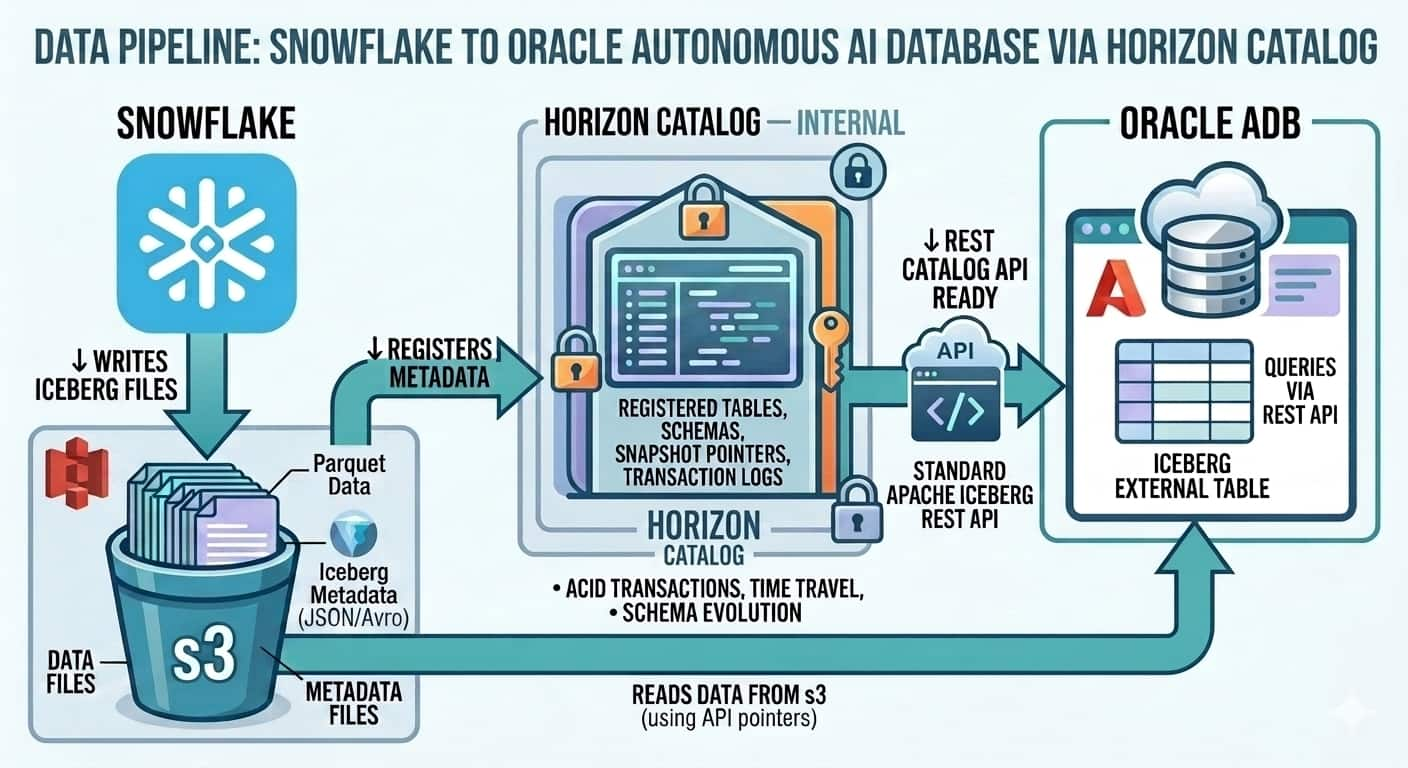

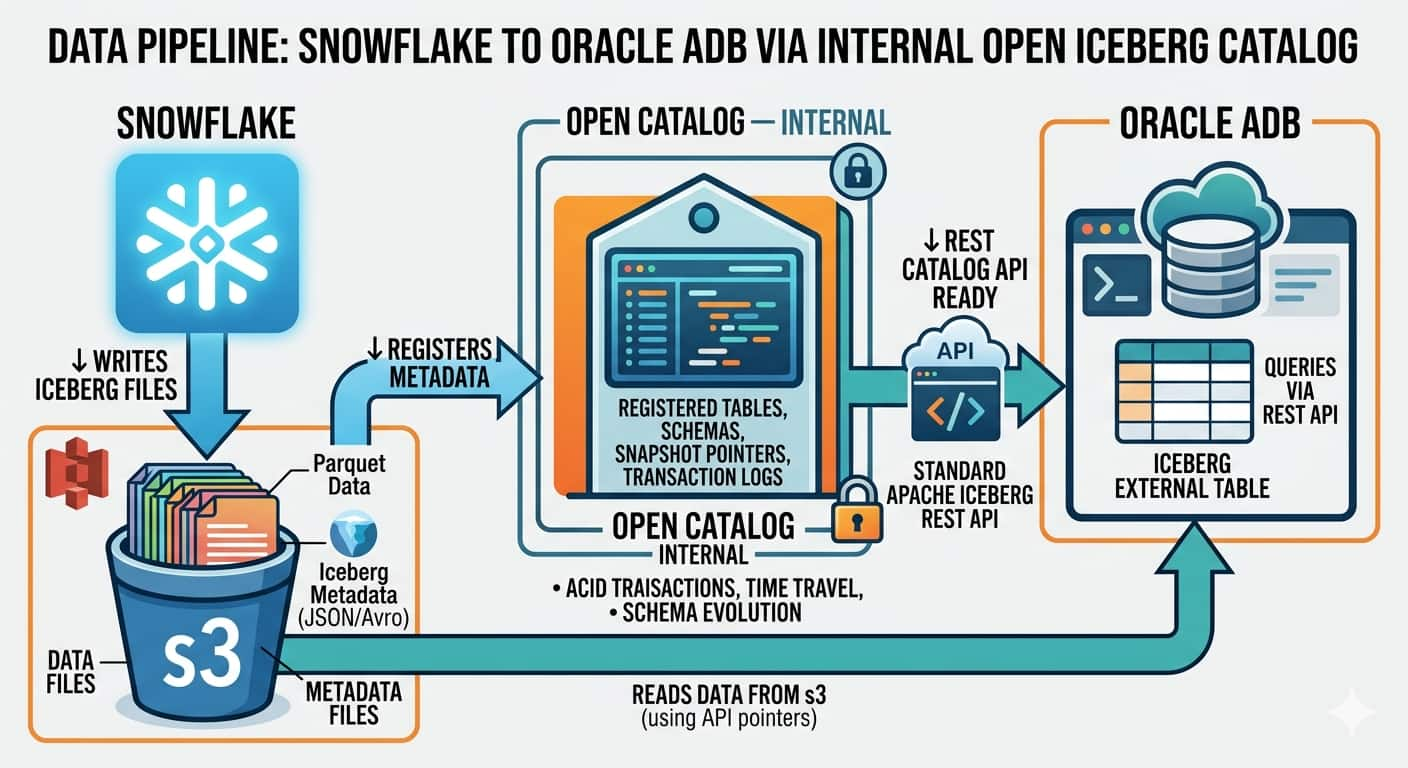

Bridging Oracle Autonomous AI Database and Snowflake: Reading Iceberg ...

Sathishkumar Rangaraj

8 minute read

Turning Invoice Compliance into a Scalable, Auditable Workflow with ...

Kumar G Varun

6 minute read

One Zero Bank Builds a Trusted Analytics Foundation for Digital ...

Sergiu Popovici

Reiner Zimmermann

3 minute read

Streamlining Your Path to Autonomous AI Database: Migration ...

German Viscuso

2 minute read

Announcing Oracle Autonomous AI Vector Database Limited Availability

Brian Macdonald

3 minute read

AppDev

See all

Build AI Agents on Enterprise-Grade Data–With Zero License Cost

Leo Alvarado

Tammy Bednar

5 minute read

Introducing Oracle Backend for Firebase: Build Mobile and Web Apps on ...

Killian Lynch

Dominic Giles

6 minute read

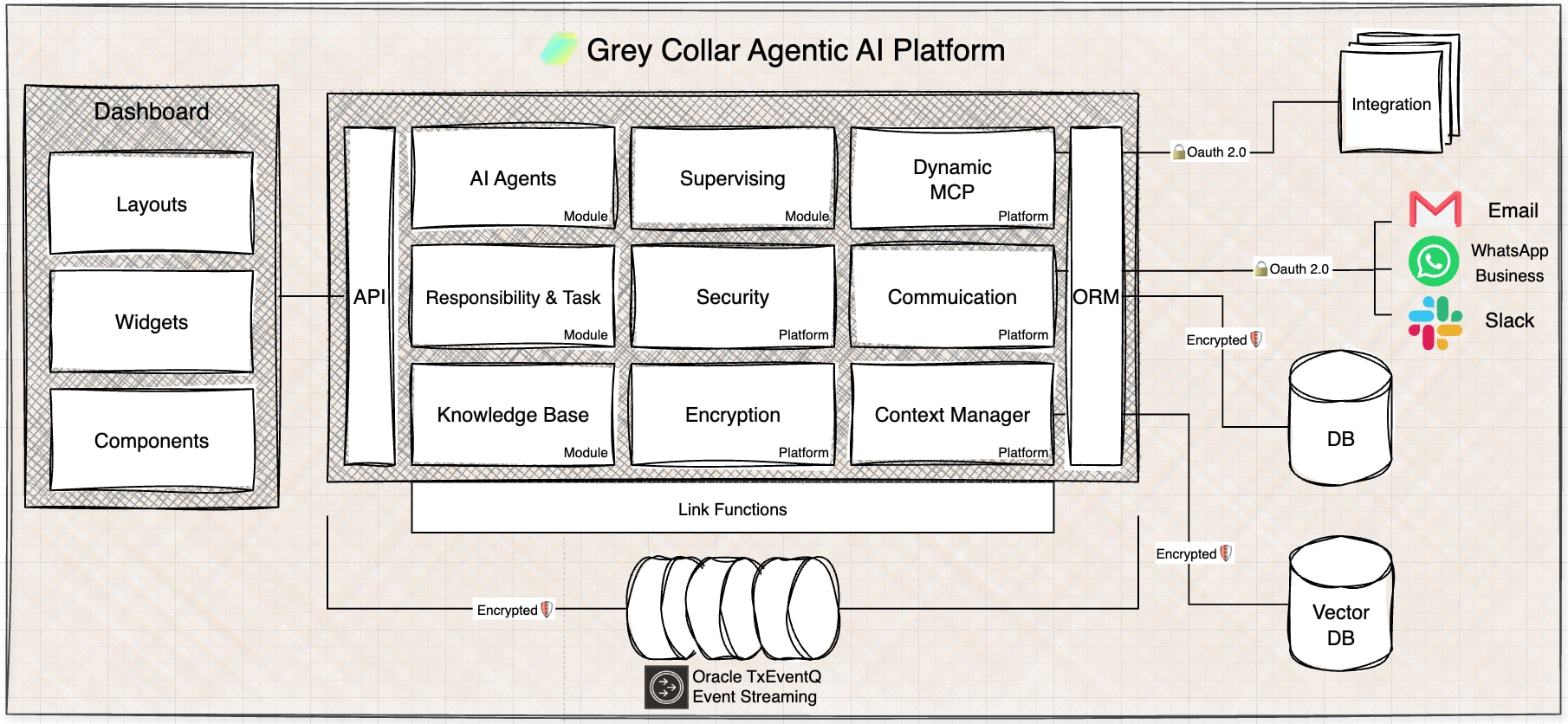

GreyCollar.ai moved agent messaging into Oracle Transactional Event ...

Anders Swanson

Nithin Thekkupadam Narayanan

5 minute read

Gain Agentic Access to Any Oracle Database in the Cloud with Native, ...

Jeff Smith

Kris Rice

8 minute read

Pain Free Vector similarity search for your apps: Oracle Database ...

Chris Hoina

9 minute read

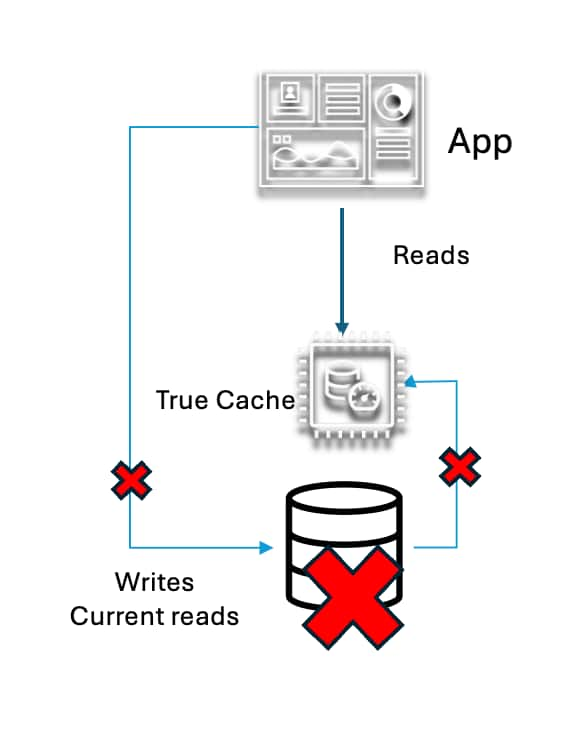

Maintain Application Read Availability as a bonus from Oracle True ...

Ilam Siva

5 minute read

Secure Agents, Built for the Enterprise

Allen Hosler

4 minute read

Eliminating Kafka Brokers with Oracle Transactional Event Queues for ...

Nithin Thekkupadam Narayanan

3 minute read

Analytics and Data Warehousing

See all

Cross-Platform Analytics: Oracle Autonomous AI Database Reads ...

Sathishkumar Rangaraj

9 minute read

Bridging Oracle Autonomous AI Database and Snowflake: Reading Iceberg ...

Sathishkumar Rangaraj

8 minute read

One Zero Bank Builds a Trusted Analytics Foundation for Digital ...

Sergiu Popovici

Reiner Zimmermann

3 minute read

Oracle Autonomous AI Lakehouse

Guest Author

5 minute read

Create Graph Databases with Graph Studio

Denise Myrick

3 minute read

Graph Database Use Cases for Financial Services Companies

Denise Myrick

4 minute read

Microsoft Azure and Oracle Database on OCI: A Big Win for Users

Guest Author

4 minute read

Why should you use graph analytics?

Neelima Tadikonda

5 minute read

Customer Stories

See all

AIOS develops customized reporting and planning solutions with Oracle ...

Martina Keippel

3 minute read

VakifBank migrates to Exadata next-gen infrastructure

Dana Serb

Kellsey Ruppel

3 minute read

Accelerating My Journey Building Enterprise AI Agents

Sanjay Goil

3 minute read

DZ Bank Accelerates Modernization and Data Protection with Oracle ...

Dana Serb

3 minute read

How Tawuniya tamed data management costs with Oracle ILM and Advanced ...

Maria Colgan

Peter Schutt

3 minute read

DeweyVision Transforms Media Discovery with Oracle AI Vector Search: ...

Malu Castellanos

6 minute read

Cummins in India uses Oracle Database Security to help meet ...

Viral Patel

Jeevan Pandit

Angeline Dhanarani

6 minute read

Umm Al-Qura University Meets Data Privacy and Data Protection ...

Mohannad Aljammal

Pedro Lopes

2 minute read

Database Cloud Services

See all

Build AI Agents on Enterprise-Grade Data–With Zero License Cost

Leo Alvarado

Tammy Bednar

5 minute read

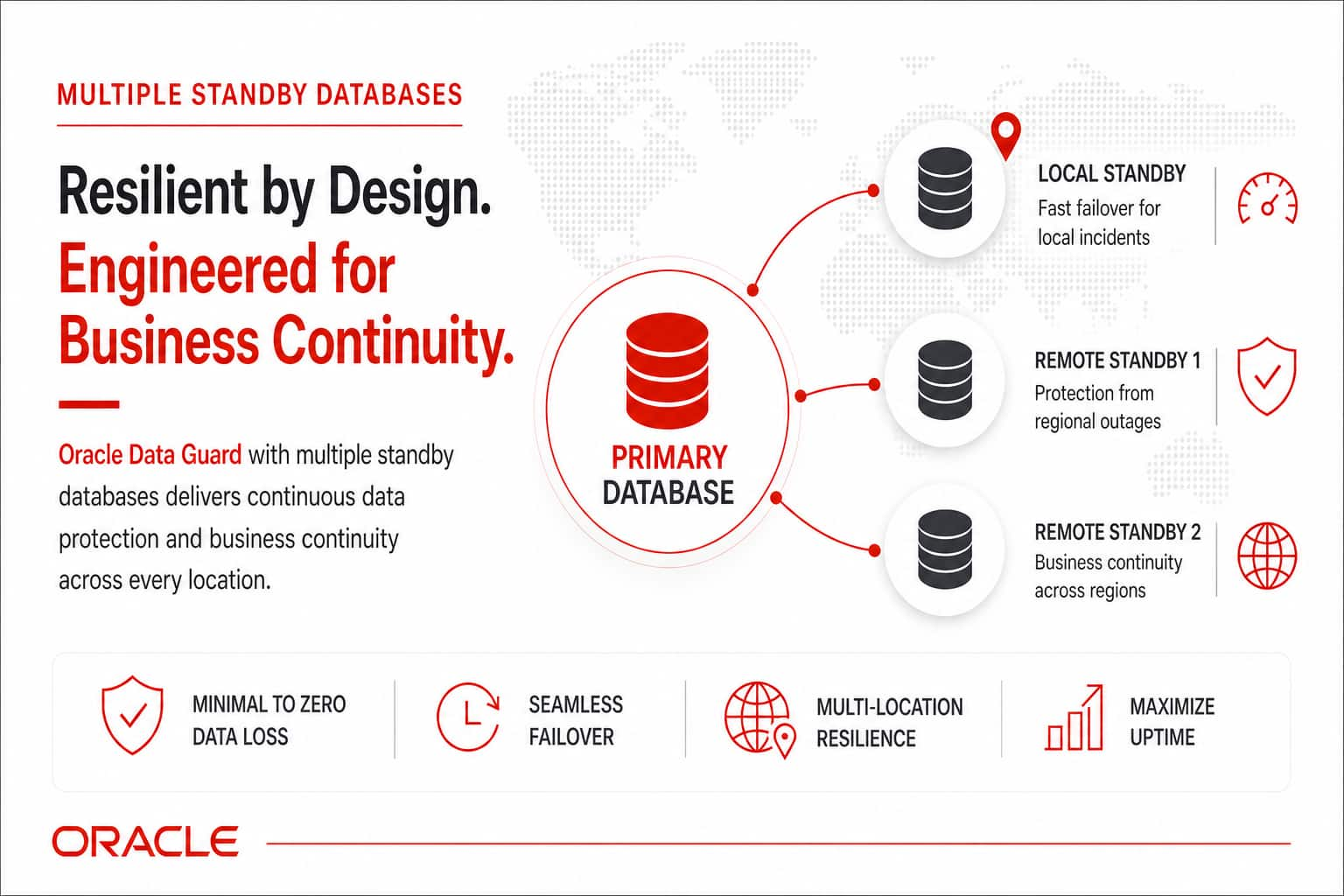

Modernize Your Disaster Recovery Strategy: Multiple Standby databases ...

Dileep Thiagarajan

Leo Alvarado

5 minute read

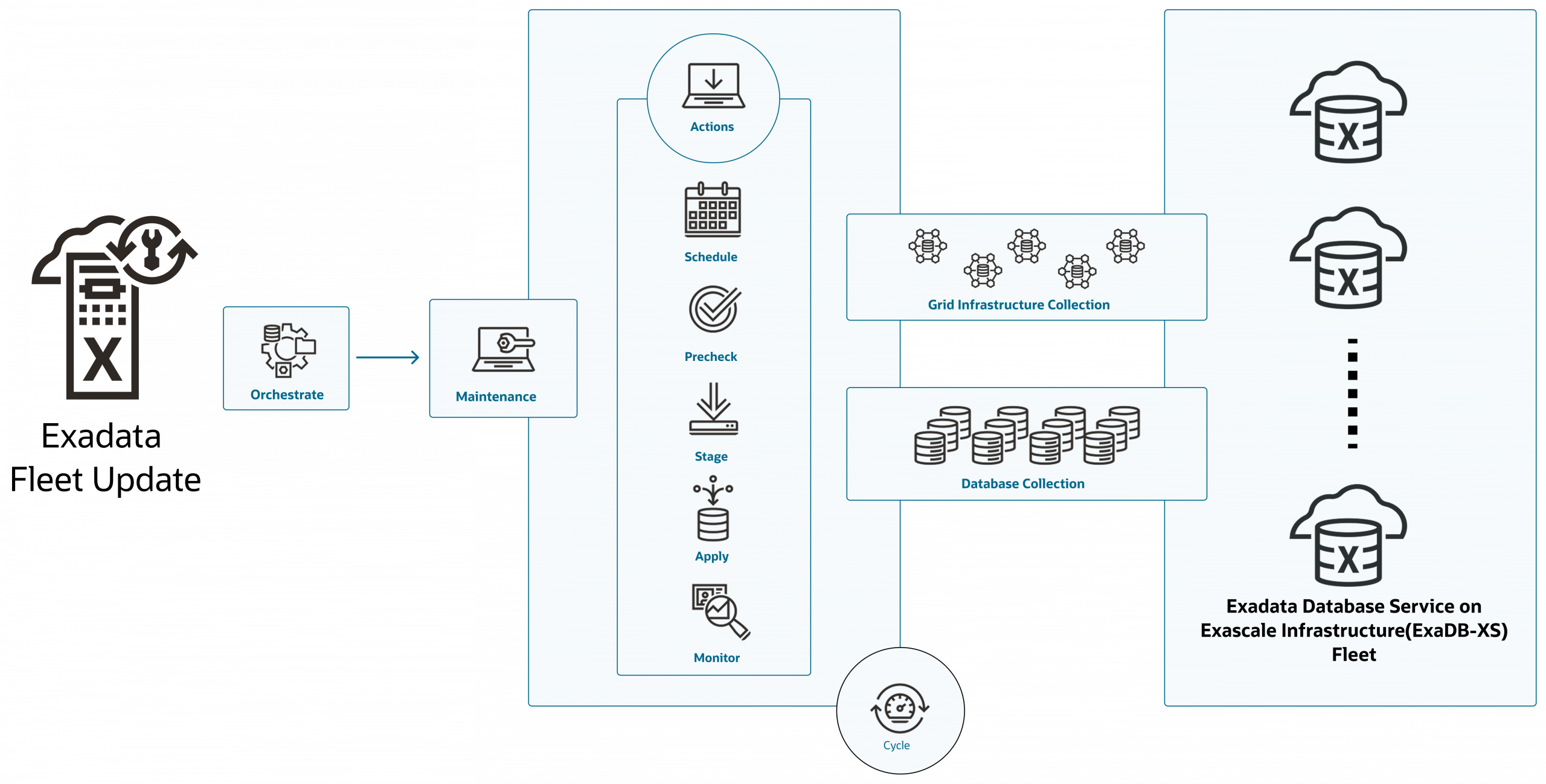

Announcing Exadata Fleet Update support for Exadata Database Service ...

Vishal Patil

Prince Mathew

3 minute read

Announcing the Extreme Flash Storage Server for Exadata Cloud@Customer

Kevin Deihl

2 minute read

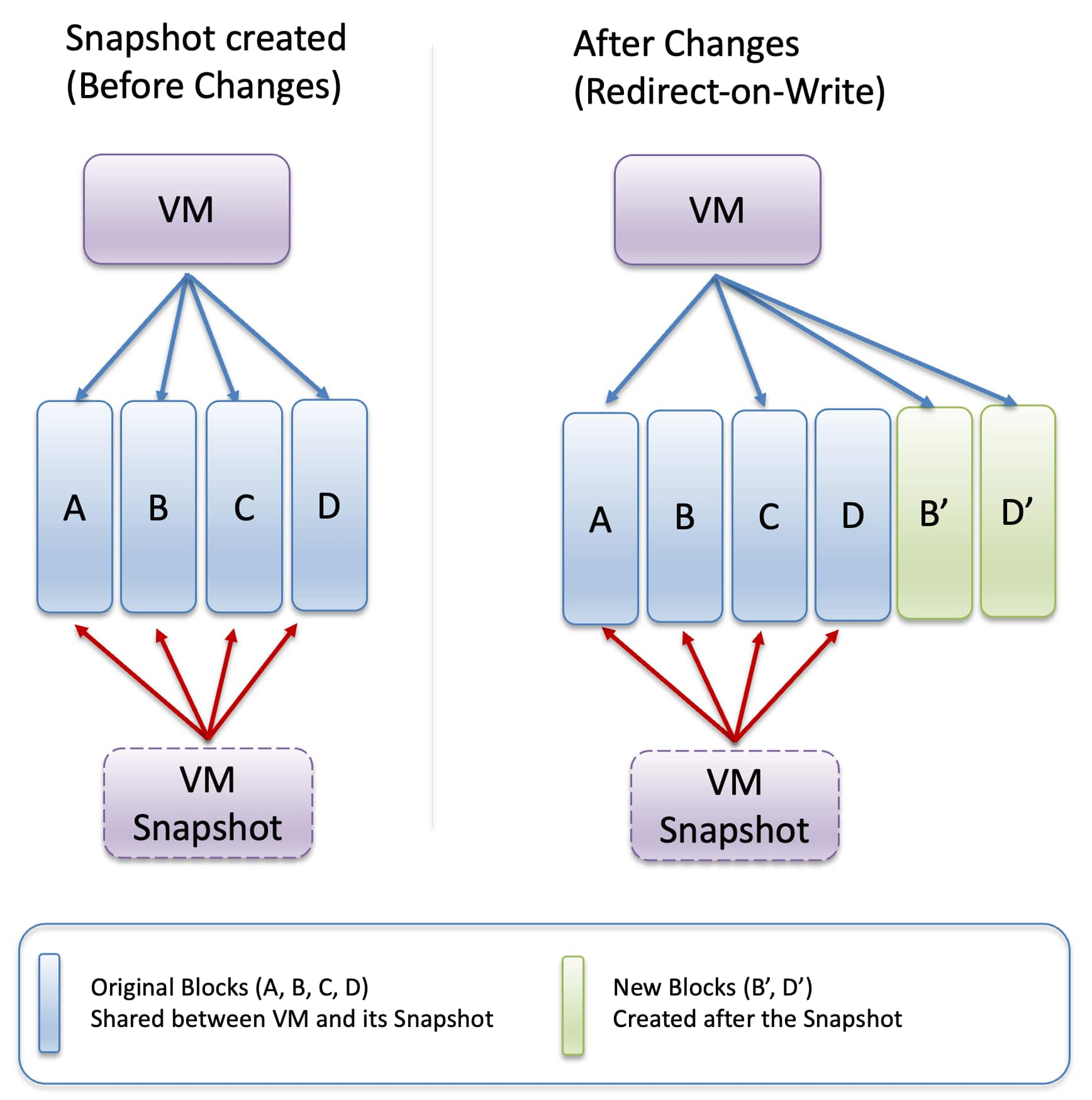

Introducing On‑Demand VM Snapshots for Oracle Exadata Database ...

Deepika Pandhi

5 minute read

Maintain Application Read Availability as a bonus from Oracle True ...

Ilam Siva

5 minute read

Secure Agents, Built for the Enterprise

Allen Hosler

4 minute read

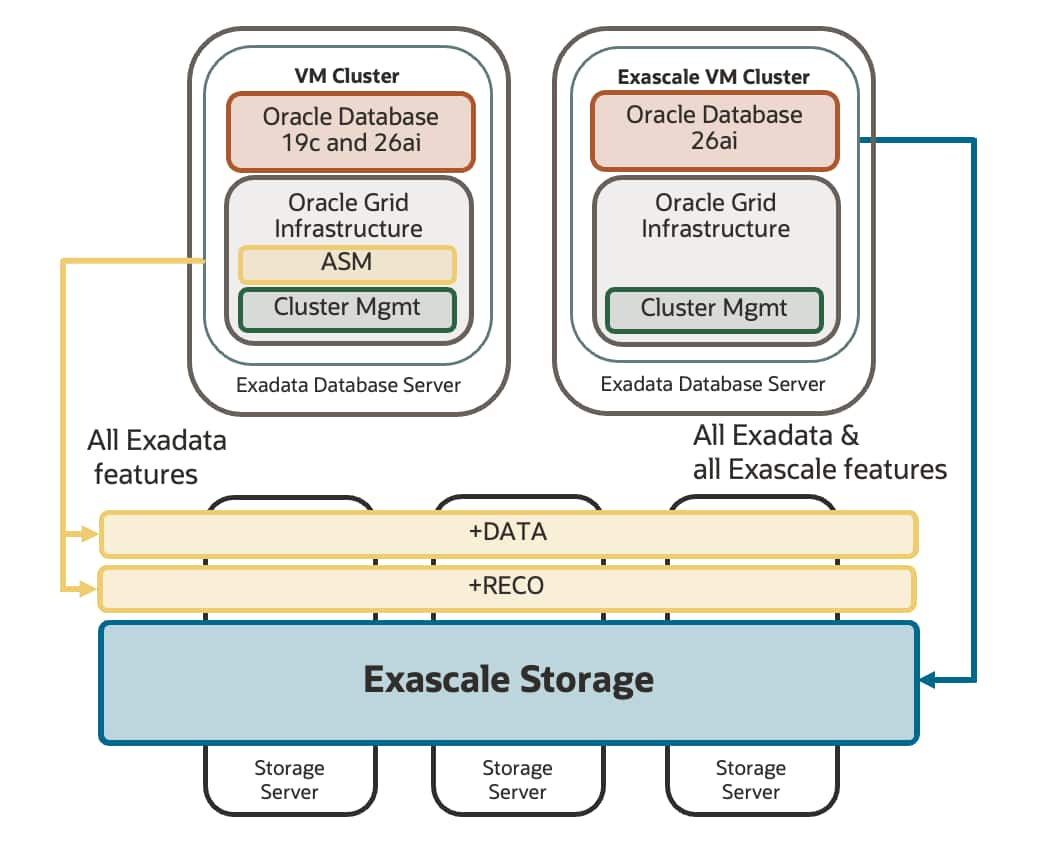

Exascale: Oracle Database Storage in the Age of the Cloud

Nathan Fuzi

7 minute read

Distributed Database

See all

Getting Started with the Vector Index Service – Part 2

Doug Hood

12 minute read

Getting Started with the Vector Index Service – Part 1

Doug Hood

15 minute read

Introducing the Vector Index Service

Doug Hood

3 minute read

From HA to Multi-Region: Always-On Distributed Databases with ...

Pankaj Chandiramani

Deeksha Sehgal

5 minute read

Maintain Application Read Availability as a bonus from Oracle True ...

Ilam Siva

5 minute read

Building Scalable Vector Search with Oracle Globally Distributed ...

Kuldeep Bora

Kehinde Otubamowo

Deeksha Sehgal

7 minute read

Oracle AI Vector Search on Globally Distributed Databases

Pankaj Chandiramani

Deeksha Sehgal

6 minute read

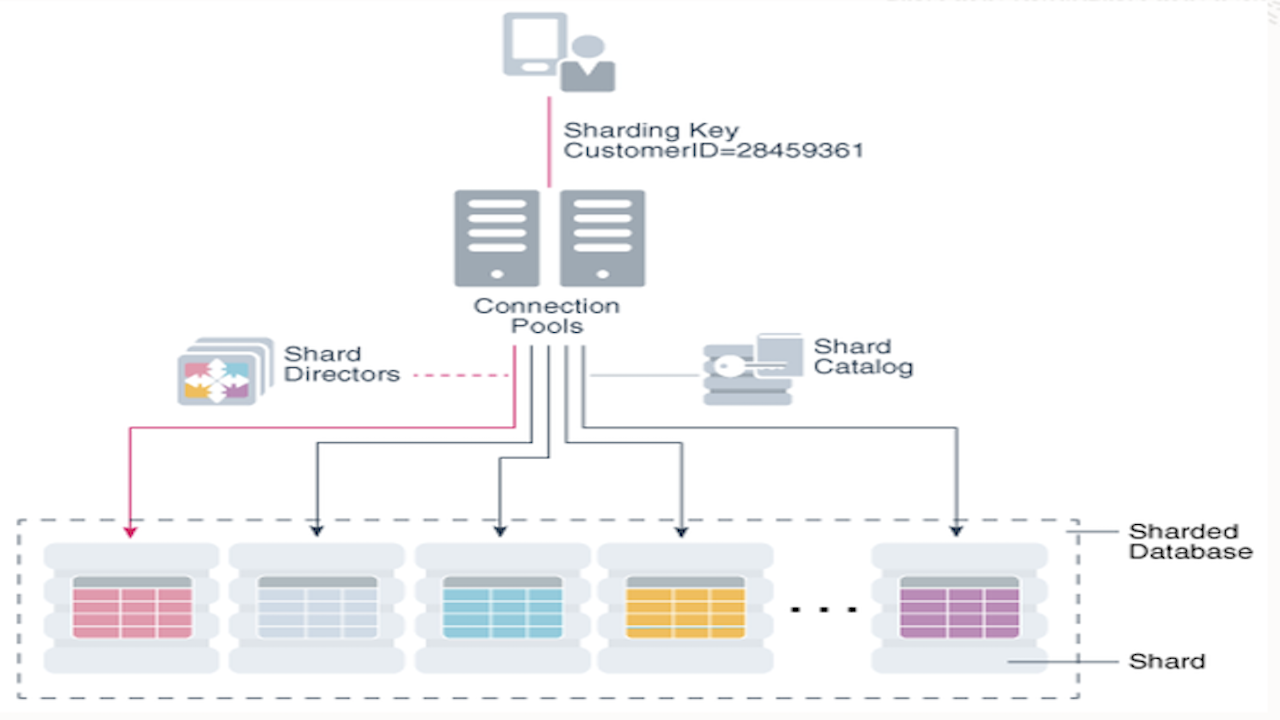

Oracle Sharding: Enterprise-Grade Distributed Database

Deeksha Sehgal

6 minute read

Engineered Systems

See all

Getting Started with the Vector Index Service – Part 2

Doug Hood

12 minute read

VakifBank migrates to Exadata next-gen infrastructure

Dana Serb

Kellsey Ruppel

3 minute read

DZ Bank Accelerates Modernization and Data Protection with Oracle ...

Dana Serb

3 minute read

Intelligent Data Storage? – Deal Me In!

Steve Kilgore

2 minute read

Oracle Key Vault is now available on Oracle Database Appliance

Peter Wahl

4 minute read

Run Oracle True Cache on-premise with Oracle Database Appliance (ODA)

Ilam Siva

4 minute read

Don’t Be Fooled by Misleading Data Egress Announcements

Steve Kilgore

10 minute read

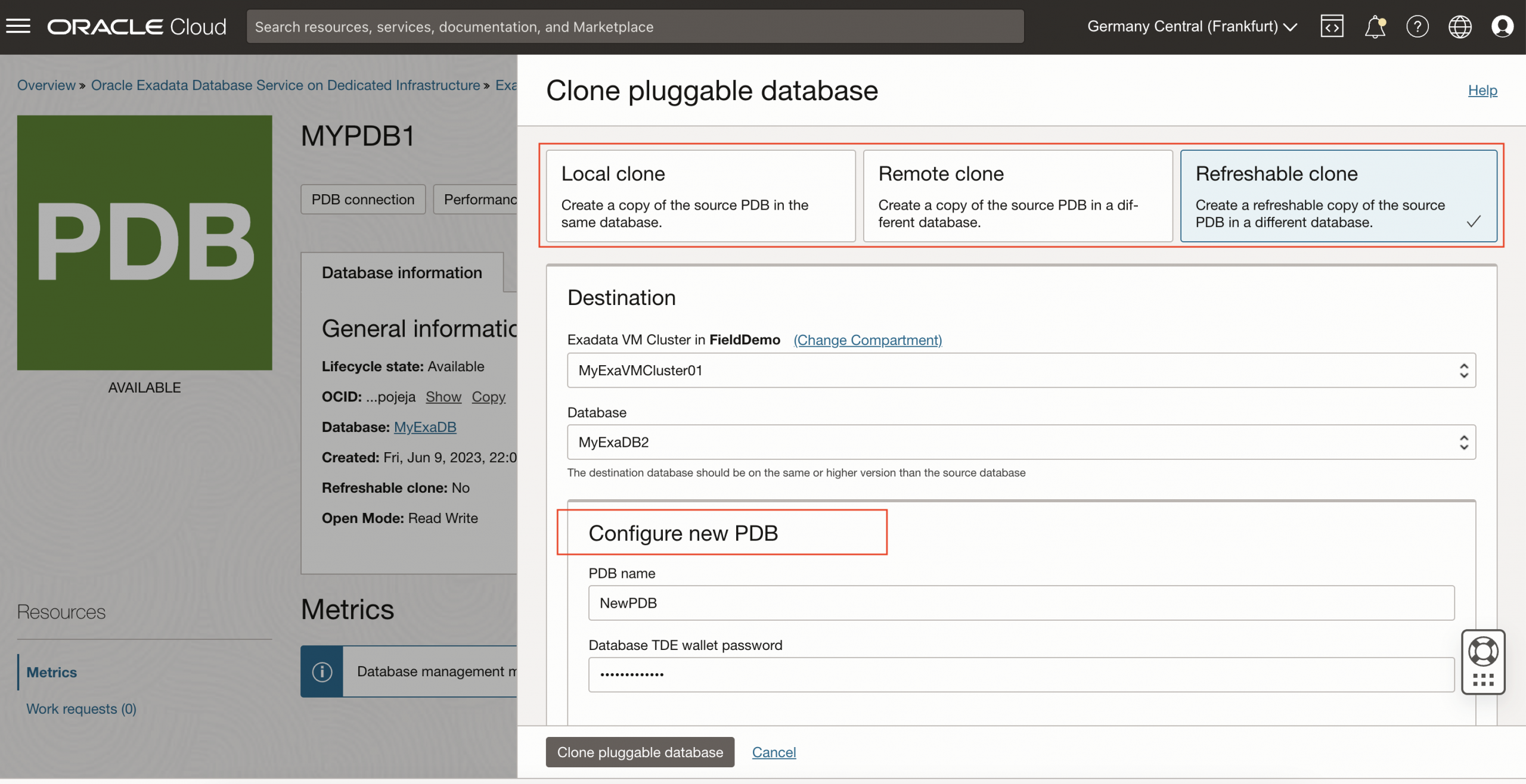

Enhanced PDB automation on Exadata and Base Database Services

Pravin Jha

7 minute read

Graph

See all

Automate Graph Creation with Generative AI

Melliyal Annamalai

4 minute read

Leading Industry Analysts Comment on the Latest AI and Machine ...

Youko Watari

4 minute read

New! Discover connections with SQL Property Graphs in Oracle ...

Marty Gubar

Jayant Sharma

3 minute read

Oracle Graph Learning Path

Rahul Tasker

5 minute read

Graph RAG: Bring the Power of Graphs to Generative AI

Melliyal Annamalai

5 minute read

Join us for Analytics and Data Summit 2023, March 14-16, Redwood ...

Jean Ihm

2 minute read

Graph Analytics for All of Your Data

Melliyal Annamalai

7 minute read

Third Quarterly Update On Oracle Graph (2025)

Rahul Tasker

6 minute read

High Availability

See all

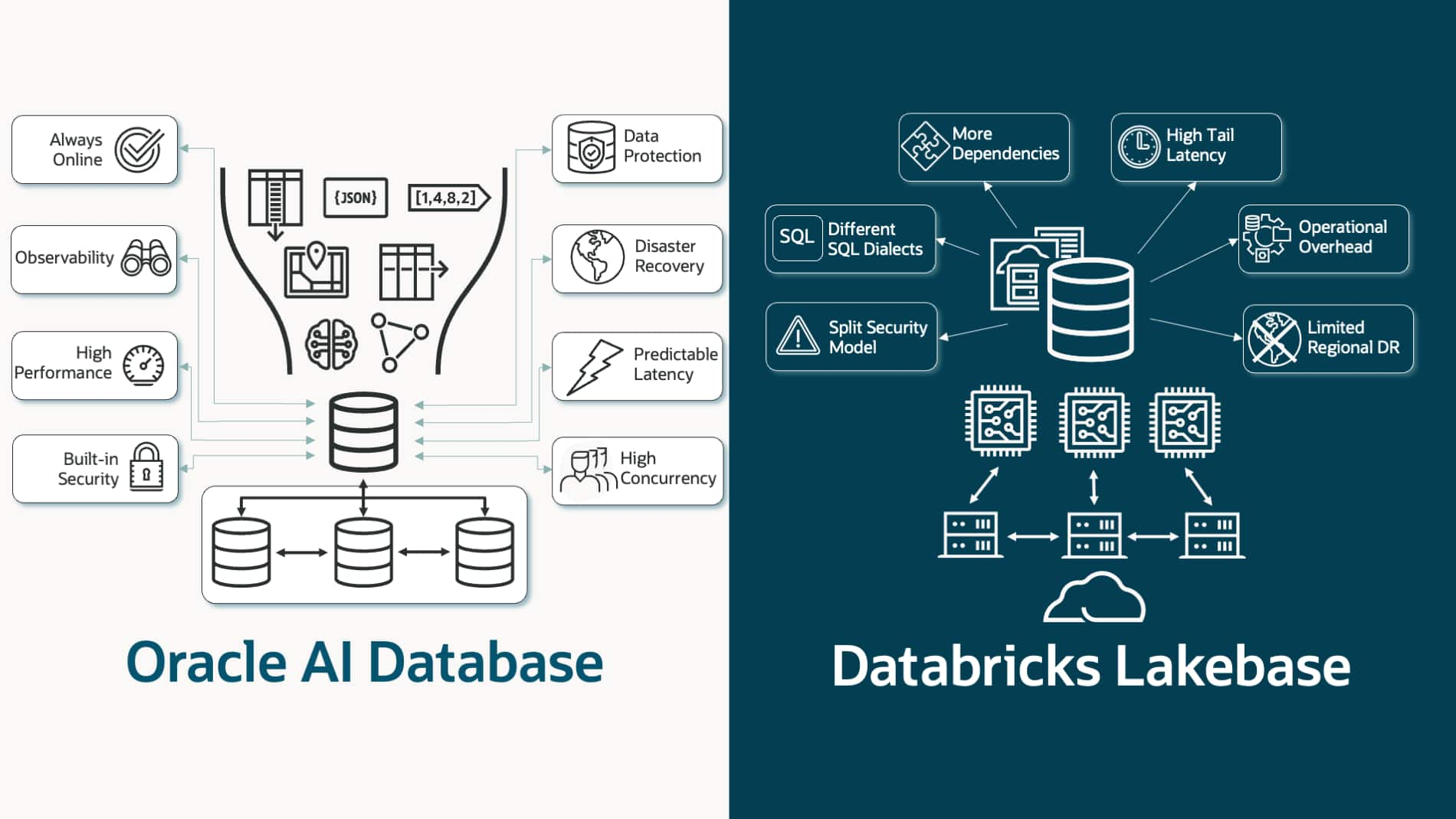

Oracle AI Database vs Databricks Lakebase for Modern OLTP

Ludovico Caldara

14 minute read

Modernize Your Disaster Recovery Strategy: Multiple Standby databases ...

Dileep Thiagarajan

Leo Alvarado

5 minute read

Analyst Perspectives on Oracle AI Database Mission-Critical ...

Ron Craig

7 minute read

Raising the Standard for Mission-Critical Availability and Security ...

Ashish Ray

11 minute read

Maintain Application Read Availability as a bonus from Oracle True ...

Ilam Siva

5 minute read

Oracle AI Vector Search on Globally Distributed Databases

Pankaj Chandiramani

Deeksha Sehgal

6 minute read

VakifBank migrates to Exadata next-gen infrastructure

Dana Serb

Kellsey Ruppel

3 minute read

Cross-Region High Availability for MongoDB API on OCI: Testing with ...

Burak Akkus

Corina Todea

8 minute read

JSON

See all

Cross-Region High Availability for MongoDB API on OCI: Testing with ...

Burak Akkus

Corina Todea

8 minute read

Cross-Region Active-Active Resilience for MongoDB API: Zero Downtime ...

Burak Akkus

Corina Todea

7 minute read

Cross-Region High Availability for MongoDB API on OCI: Testing with ...

Burak Akkus

Corina Todea

28 minute read

Cross-Region Active-Active Goldengate Deployment Step By Step Guide

Burak Akkus

Corina Todea

9 minute read

From SQL to GraphQL: Exploring Native GraphQL Support in Oracle AI ...

Sathishkumar Rangaraj

6 minute read

Native GraphQL in Oracle AI Database 26ai: A New Era of ...

Sathishkumar Rangaraj

3 minute read

SODA with partitioning

Maxim Orgiyan

6 minute read

Get Started with Autonomous JSON Database

Marty Gubar

Keith Laker

3 minute read

Performance

See all

Getting Started with the Vector Index Service – Part 2

Doug Hood

12 minute read

Getting Started with the Vector Index Service – Part 1

Doug Hood

15 minute read

Introducing the Vector Index Service

Doug Hood

3 minute read

Maintain Application Read Availability as a bonus from Oracle True ...

Ilam Siva

5 minute read

VakifBank migrates to Exadata next-gen infrastructure

Dana Serb

Kellsey Ruppel

3 minute read

Unveiling the Power of Oracle Globally Distributed Database: Oracle ...

Deeksha Sehgal

8 minute read

Oracle Transactional Event Queues (TxEventQ): Scalable Messaging ...

Ben Kocabasoglu

6 minute read

Oracle True Cache – AI World Round-Up + Get Hands On

Ilam Siva

4 minute read

Security

See all

Building Trusted Generative AI Experiences with Oracle Deep Data ...

Burak Akkus

14 minute read

India Privacy Act DPDPA, AI Threats, and Quantum Risks All Converge ...

David Knox

7 minute read

Getting Started with the Vector Index Service – Part 2

Doug Hood

12 minute read

Getting Started with the Vector Index Service – Part 1

Doug Hood

15 minute read

Oracle Deep Data Security Is Now Available in Oracle AI Database 26ai

Vipin Samar

5 minute read

Raising the Standard for Mission-Critical Availability and Security ...

Ashish Ray

11 minute read

Introducing Oracle Database Security Central: Taking Control of ...

Vipin Samar

4 minute read

Introducing Oracle Deep Data Security: Identity-Aware Data Access ...

Roger Wigenstam

3 minute read

Spatial

See all

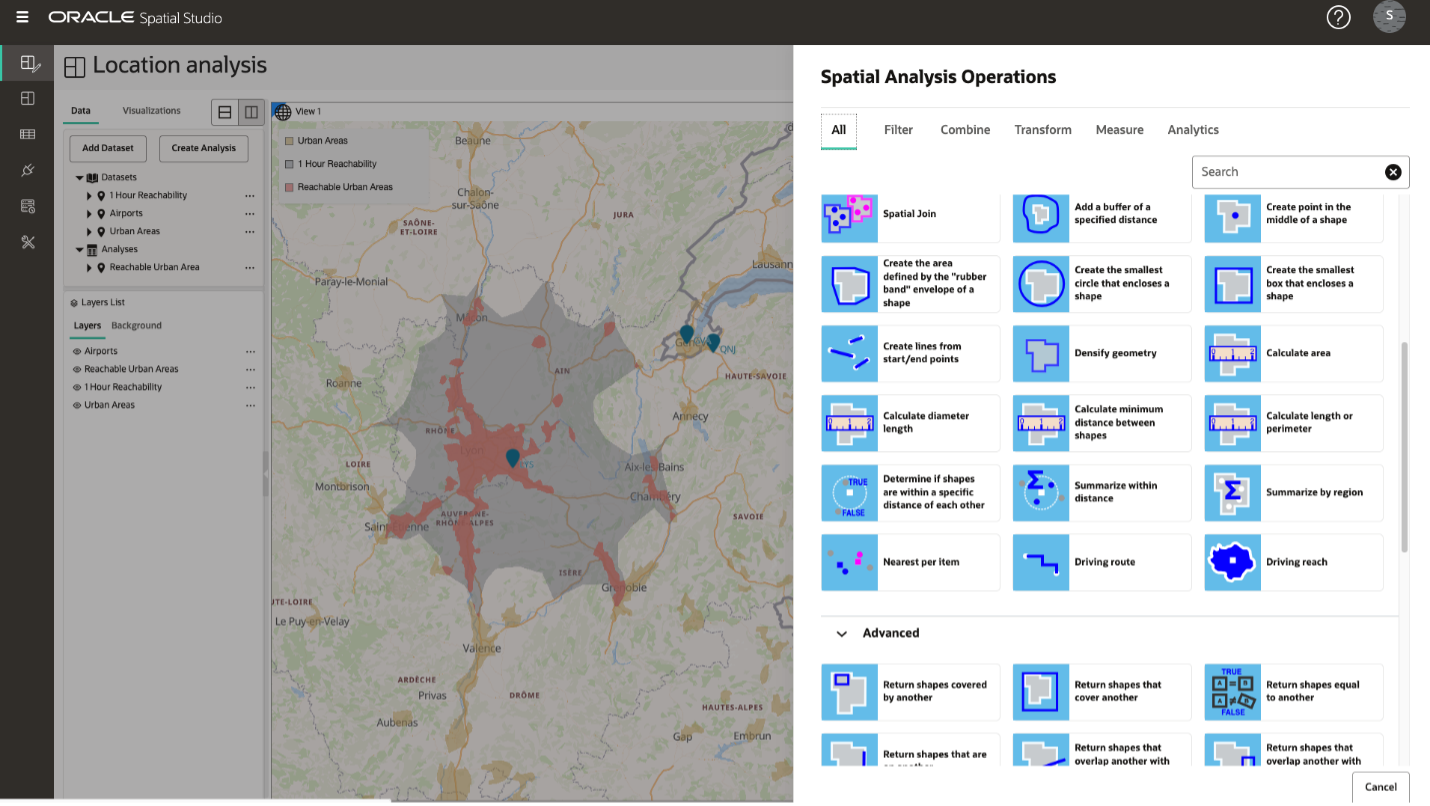

Unlock Spatial Insights Faster with Spatial Studio, Now Built into ...

David Lapp

4 minute read

Accelerating Geospatial Innovation with CARTO on Oracle Autonomous AI ...

Hans Viehmann

5 minute read

Leading Industry Analysts Comment on the Latest AI and Machine ...

Youko Watari

4 minute read

Join us for Analytics and Data Summit 2023, March 14-16, Redwood ...

Jean Ihm

2 minute read

What’s new in Oracle Spatial Studio 25.1

Denise Myrick

2 minute read

Oracle named to Geoawesome’s Global Top 100 Geospatial Companies 2025 ...

Youko Watari

Jean Ihm

3 minute read

Optimize Streaming Map Data with Vector Tile Cache in Oracle Spatial

Rahul Tasker

3 minute read

Spatial Studio 24.2 Now Available

Denise Myrick

2 minute read

Autonomous Health Framework

See all

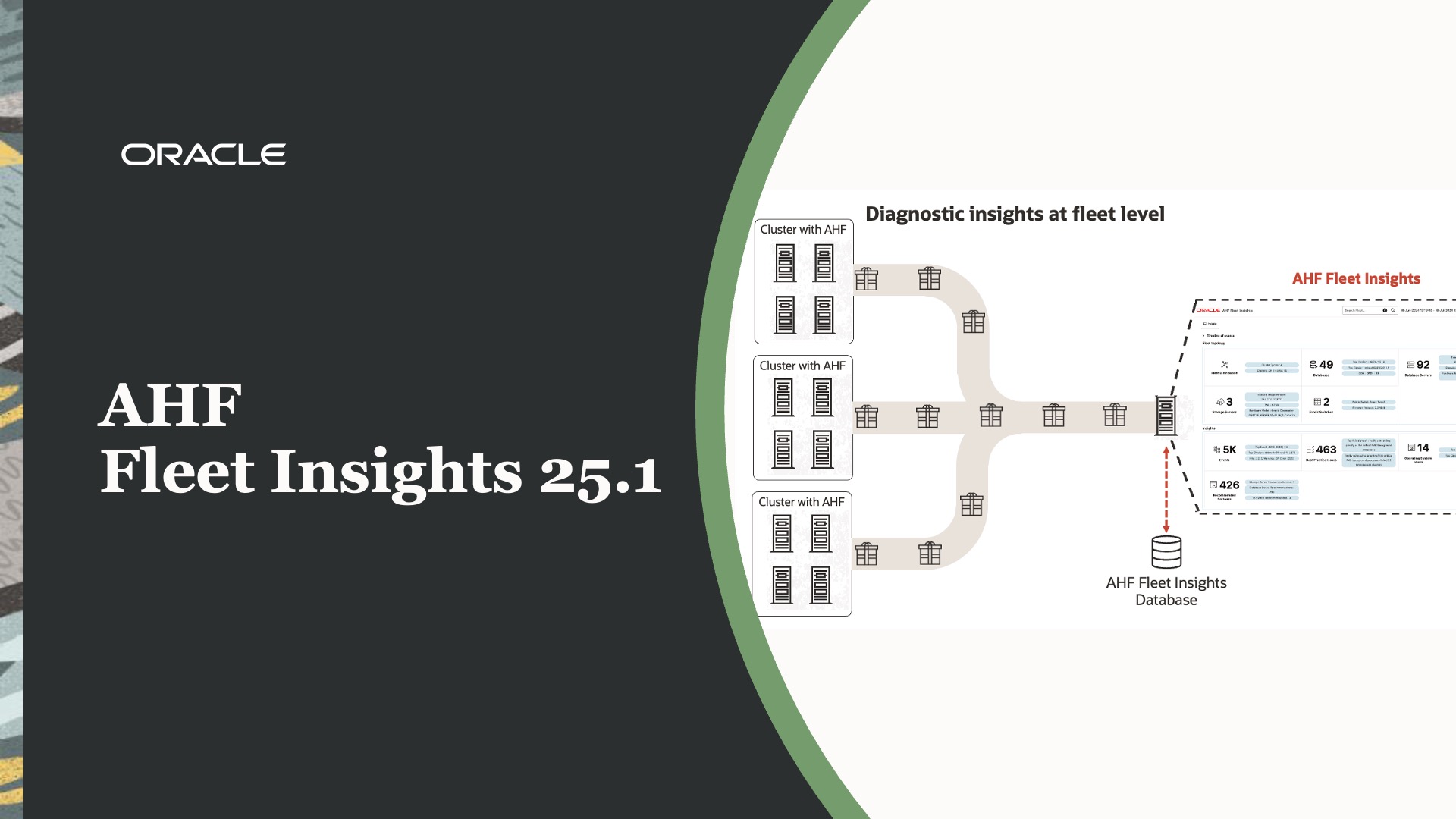

AHF Fleet Insights 25.1 with Single-Instance Support and More!

Gareth Chapman

4 minute read

AHF Fleet Insights 25.2 with AI powered Capacity Analysis and ...

Rohini Ramadath

7 minute read

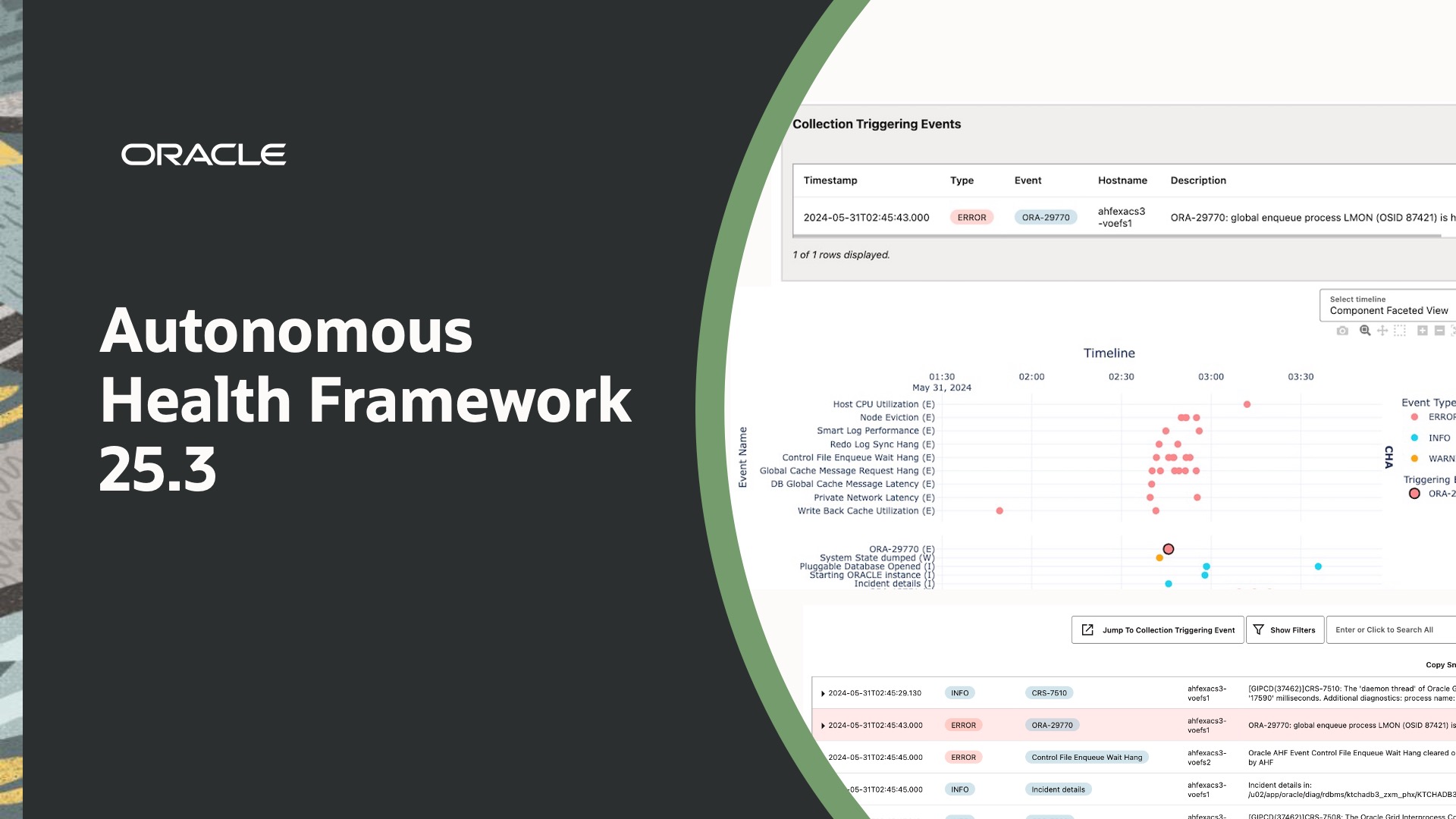

Explore Diagnostic Collections Triggering Events with AHF 25.3

Gareth Chapman

5 minute read

Support for Exadata X11M and Exadata System Software 25.1 with AHF ...

Gareth Chapman

5 minute read

Maximizing Application Resilience, Performance, and Security with AHF ...

Gareth Chapman

11 minute read

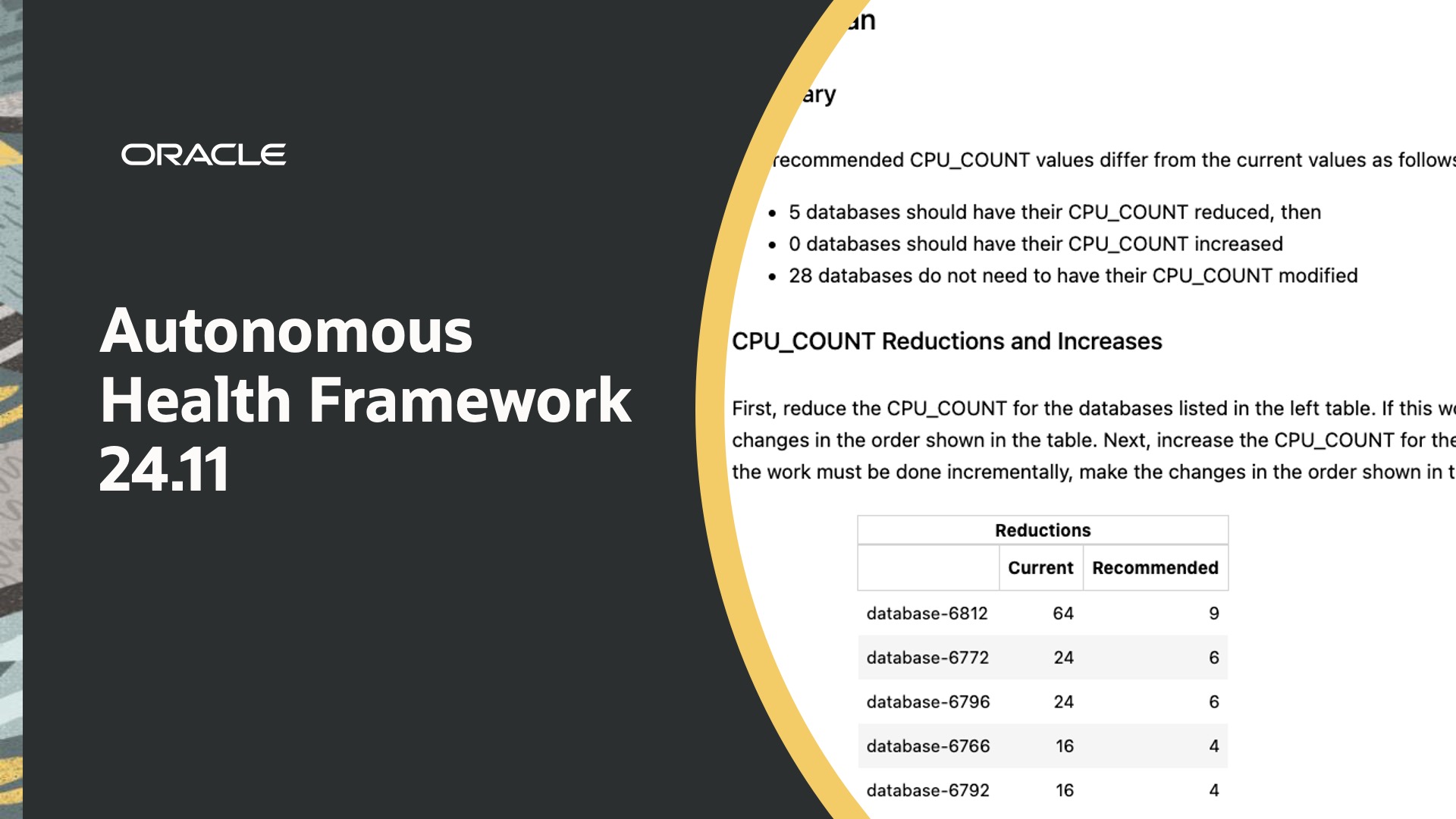

Optimize Database Performance and Hardware Usage with AHF 24.11

Gareth Chapman

5 minute read

New Automatic Solutions for Node Eviction with AHF 24.10

Gareth Chapman

6 minute read

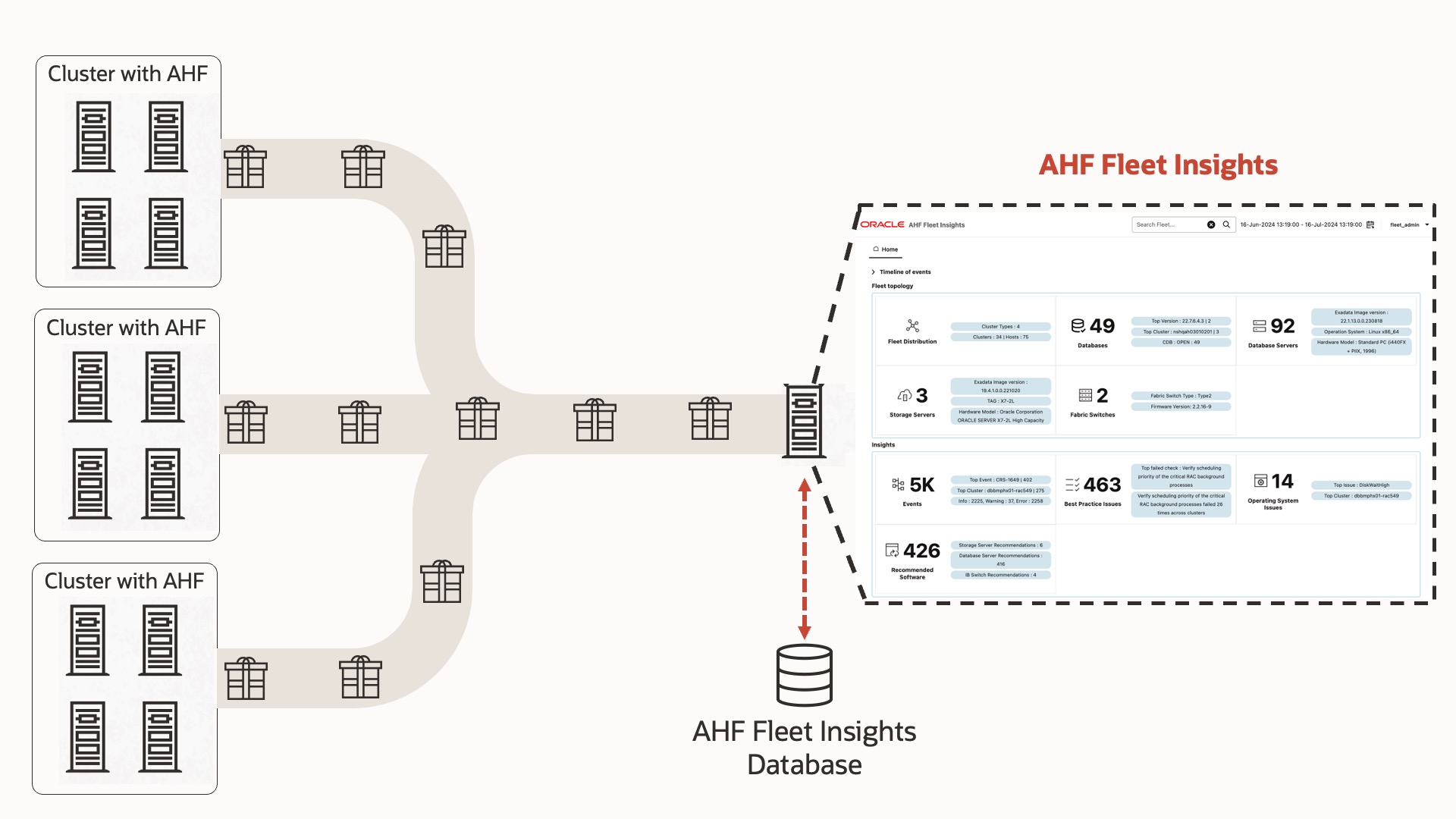

Introducing AHF Fleet Insights

Gareth Chapman

3 minute read

Select AI

See all

Building Trusted Generative AI Experiences with Oracle Deep Data ...

Burak Akkus

14 minute read

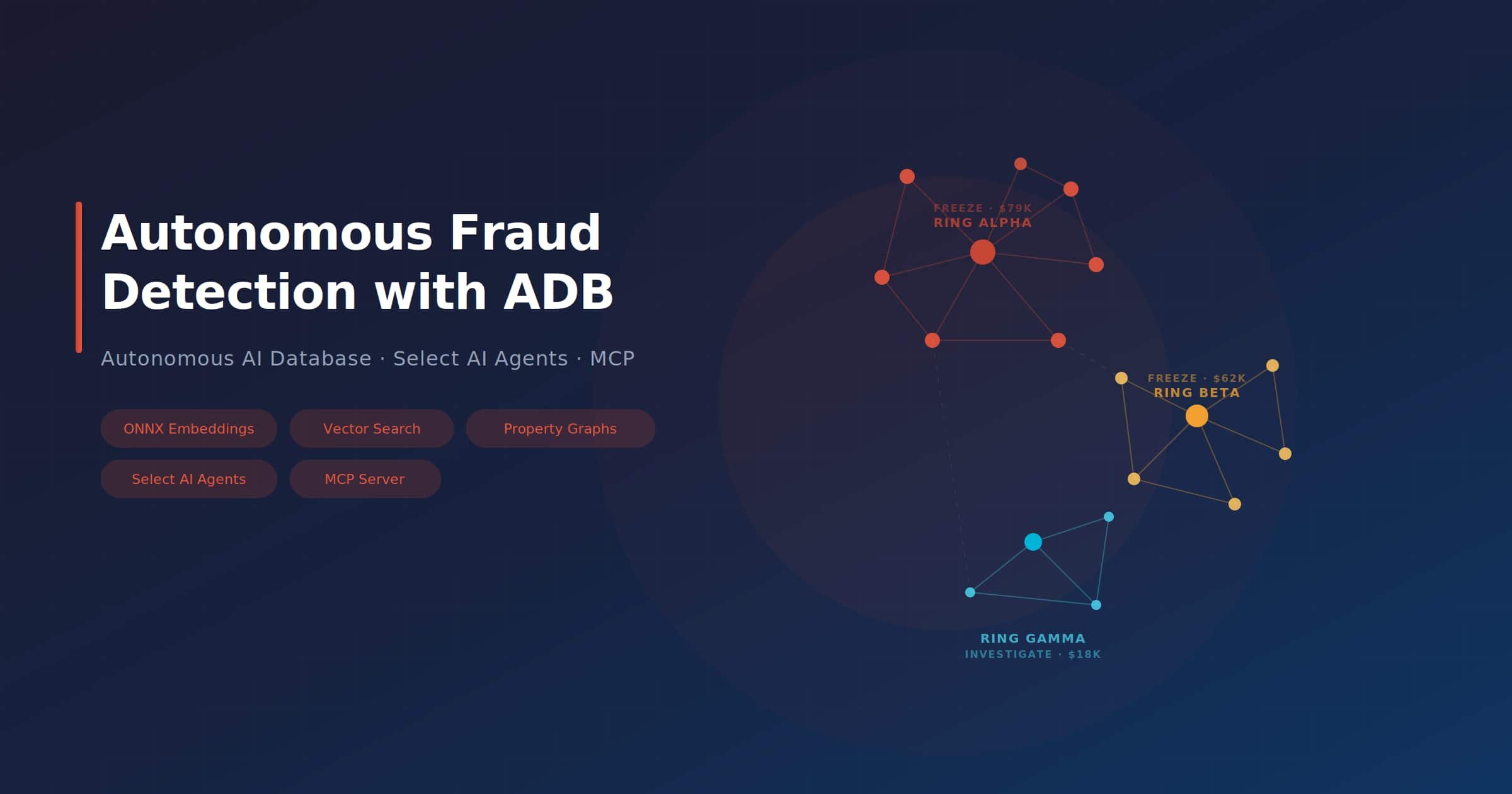

Building an Autonomous Fraud Detection Pipeline with Autonomous AI ...

German Viscuso

10 minute read

Autonomous AI Database

See all

Building Trusted Generative AI Experiences with Oracle Deep Data ...

Burak Akkus

14 minute read

Cross-Platform Analytics: Oracle Autonomous AI Database Reads ...

Sathishkumar Rangaraj

9 minute read

Bridging Oracle Autonomous AI Database and Snowflake: Reading Iceberg ...

Sathishkumar Rangaraj

8 minute read

Turning Invoice Compliance into a Scalable, Auditable Workflow with ...

Kumar G Varun

6 minute read

Building an Autonomous Fraud Detection Pipeline with Autonomous AI ...

German Viscuso

10 minute read

Enterprise AI Search Needs a New Approach

Allen Hosler

4 minute read

Oracle AI

See all

Building Trusted Generative AI Experiences with Oracle Deep Data ...

Burak Akkus

14 minute read

The Resurgence of No-Code

Allen Hosler

6 minute read

Cross-Platform Analytics: Oracle Autonomous AI Database Reads ...

Sathishkumar Rangaraj

9 minute read

Oracle AI Database Private Agent Factory: Enterprise FAQ

Kumar G Varun

10 minute read

Turning Invoice Compliance into a Scalable, Auditable Workflow with ...

Kumar G Varun

6 minute read

Technical Solutions

See all

Cross-Platform Analytics: Oracle Autonomous AI Database Reads ...

Sathishkumar Rangaraj

9 minute read

Bridging Oracle Autonomous AI Database and Snowflake: Reading Iceberg ...

Sathishkumar Rangaraj

8 minute read

Receive the latest blog updates

Subscribe to our blog

Resources for

About

Careers

Developers

Investors

Partners

Startups

Why Oracle

Analyst Reports

Best CRM

Cloud Economics

Corporate Responsibility

Security Practices

Learn

What is Customer Service?

What is ERP?

What is Marketing Automation?

What is Procurement?

What is Talent Management?

What is VM?

What's New

Try Oracle Cloud Free Tier

Oracle Sustainability

Oracle COVID-19 Response

Oracle and SailGP

Oracle and Premier League

Oracle and Red Bull Racing Honda

Contact Us

US Sales 1.800.633.0738

How can we help?

Subscribe to Oracle Content

Try Oracle Cloud Free Tier

Events

News

© 2026 Oracle

Privacy

/

Do Not Sell My Info

Ad Choices

Careers